2.1 Social Enterprise

Although research and papers define the social enterprise(Defourny & Nyssens, 2010; Díaz-Foncea & Marcuello, 2012; Verreynne, Miles, & Harris, 2012), there is no consensus on the definition of social enterprise. One recognized and rather narrow definition is written by Professor Muhammad Yunus. According to his definition, a social enterprise is “a non-loss, non-dividend company designed to address a social objective within the highly regulated marketplace of today”(Yunus, 2007). Social enterprises are distinct from a non-profit organization because they should seek to generate a modest profit. Profit is a method to allow the business to expand its reach and improve its products or services, all of which subsidize a specific social mission.

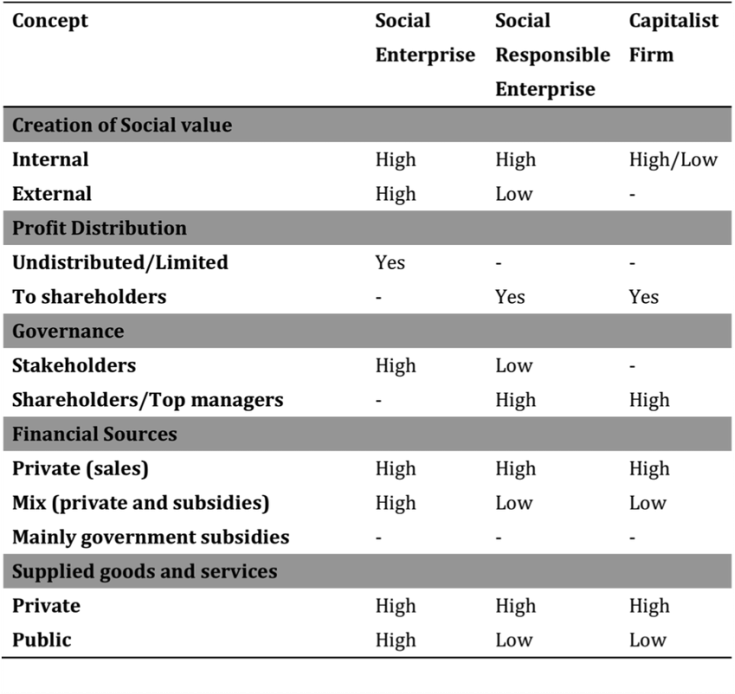

Table 1 shows which elements that define a social enterprise and draws comparison between social enterprise with the socially responsible enterprises and the capitalist firms (traditional enterprises).

Although research and papers define the social enterprise(Defourny & Nyssens, 2010; Díaz-Foncea & Marcuello, 2012; Verreynne, Miles, & Harris, 2012), there is no consensus on the definition of social enterprise. One recognized and rather narrow definition is written by Professor Muhammad Yunus. According to his definition, a social enterprise is “a non-loss, non-dividend company designed to address a social objective within the highly regulated marketplace of today”(Yunus, 2007). Social enterprises are distinct from a non-profit organization because they should seek to generate a modest profit. Profit is a method to allow the business to expand its reach and improve its products or services, all of which subsidize a specific social mission.

Table 1 shows which elements that define a social enterprise and draws comparison between social enterprise with the socially responsible enterprises and the capitalist firms (traditional enterprises).

The comparison of these factors shows that the difference between one type of organization and another is not always significant. In addition, the absence of profits or the presence of certain limitations on distribution is not enough to be considered a social enterprise. It is also necessary to assume the set of values and aims that are embodied in the business model, only with these satisfied can the business be categorized as a social enterprise(Díaz-Foncea & Marcuello, 2012).

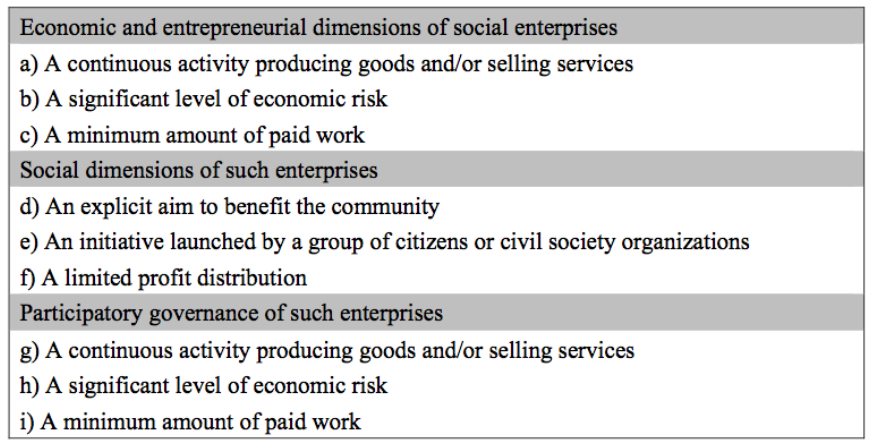

Social Economy Europe (2008) defines the social economy entities by their aims and by their distinctive forms of entrepreneurship (Monzon & Chaves, 2008). They are economic and social players active in all sectors including cooperatives, mutual

societies, associations, foundations, and social enterprises whose aims and forms agree

with the following principle:

Table 2 Social Enterprises definition, EMES

Social Economy Europe (2008) defines the social economy entities by their aims and by their distinctive forms of entrepreneurship (Monzon & Chaves, 2008). They are economic and social players active in all sectors including cooperatives, mutual

societies, associations, foundations, and social enterprises whose aims and forms agree

with the following principle:

- (1) the primacy of the individual and the social objective over capital

- (2) voluntary and open membership

- (3) democratic control by the membership

- (4) the combination of the interests of members/users and/or the general interest

- (5) the defense and application of the principle of solidarity and responsibility

- (6) autonomous management and independence from public authorities

- (7) the essential surplus is used to carry out sustainable development objectives, services of interest to members or of general interest.

Table 2 Social Enterprises definition, EMES

Note. These indicators were never intended to represent the set of conditions that an organization should meet to qualify as a social enterprise. Rather than constituting prescriptive criteria, they describe an "ideal-type" that enables researchers to position themselves in the social enterprises field.

In the U.S, Dees and Anderson (2006) have proposed to distinguish two major schools of thought on social enterprise. The first school of thought on social enterprise refers to the use of commercial activities by non-profit organizations in support of their mission. The second school of thought focuses on social innovation and social entrepreneurs(Dees & Anderson, 2006). Various foundations involved in “venture philanthropy,” such as the Schwab Foundation and the Skoll Foundation, have embraced the idea that social innovation is central to social entrepreneurship and have supported social entrepreneurs.

The Social Enterprise Knowledge Network (Harvard Business School) wrote an even wider definition of social enterprise. The network wrote the following:

"a social enterprise is any kind of enterprise and undertaking, encompassed by non-profit organization, for-profit companies or public sector businesses engaged in activities of significant social value or in the production of goods and services with an embedded social purpose(Brouard & Larivet, 2010)".

From hereon after, “social enterprise” will refer to the above definition. This definition is open and broad yet specific for the purpose necessary for constructing a social enterprise business model. Another strong point of this definition is that social enterprise is defined specifically in terms of other social organizations, e.g., non-profit organizations, for-profit organizations. Defining social enterprise in this way not only is specific but also allows for a broad and wide application. Most important, this definition of social enterprise considers both the social value and financial value of the enterprise, which is the key feature of social enterprise that I shall consider in this thesis

In the U.S, Dees and Anderson (2006) have proposed to distinguish two major schools of thought on social enterprise. The first school of thought on social enterprise refers to the use of commercial activities by non-profit organizations in support of their mission. The second school of thought focuses on social innovation and social entrepreneurs(Dees & Anderson, 2006). Various foundations involved in “venture philanthropy,” such as the Schwab Foundation and the Skoll Foundation, have embraced the idea that social innovation is central to social entrepreneurship and have supported social entrepreneurs.

The Social Enterprise Knowledge Network (Harvard Business School) wrote an even wider definition of social enterprise. The network wrote the following:

"a social enterprise is any kind of enterprise and undertaking, encompassed by non-profit organization, for-profit companies or public sector businesses engaged in activities of significant social value or in the production of goods and services with an embedded social purpose(Brouard & Larivet, 2010)".

From hereon after, “social enterprise” will refer to the above definition. This definition is open and broad yet specific for the purpose necessary for constructing a social enterprise business model. Another strong point of this definition is that social enterprise is defined specifically in terms of other social organizations, e.g., non-profit organizations, for-profit organizations. Defining social enterprise in this way not only is specific but also allows for a broad and wide application. Most important, this definition of social enterprise considers both the social value and financial value of the enterprise, which is the key feature of social enterprise that I shall consider in this thesis

2.2 The Business Model

Business model should include a company component, e.g. how a company selects customers, defines and offers products or services, plans tasks, distributes resources, changing over time, and makes profits (Slywotzky, 1996).Having research that focuses on strategic outcomes use business models as vehicle for carrying out business and keeping a business running (Mayo & Brown, 1999). In an economic perspective, a business model is a statement records how a company makes money and sustains itself over time(Stewart & Zhao, 2000).

Throughout this thesis, the definition of business model and other information associated with it generally are according to the *business model canvas proposed by Osterwalder and Pigneur (Business Model Generation 2010). Osterwalder et al. (2005) defines a business model describes the rationale of how an organization creates, delivers, and captures value. Osterwalder also asserts that business model is the blueprint of how a company does business. This definition focuses on the components of a business model that is particularly fits this research for two reasons. First, those components facilitate the innovation and discussion of social enterprise business model among entrepreneurs, investors and other stakeholders. Second, the business model canvas of Osterwalder containing nine components is a good base for a business model platform with social enterprise.

Business model should include a company component, e.g. how a company selects customers, defines and offers products or services, plans tasks, distributes resources, changing over time, and makes profits (Slywotzky, 1996).Having research that focuses on strategic outcomes use business models as vehicle for carrying out business and keeping a business running (Mayo & Brown, 1999). In an economic perspective, a business model is a statement records how a company makes money and sustains itself over time(Stewart & Zhao, 2000).

Throughout this thesis, the definition of business model and other information associated with it generally are according to the *business model canvas proposed by Osterwalder and Pigneur (Business Model Generation 2010). Osterwalder et al. (2005) defines a business model describes the rationale of how an organization creates, delivers, and captures value. Osterwalder also asserts that business model is the blueprint of how a company does business. This definition focuses on the components of a business model that is particularly fits this research for two reasons. First, those components facilitate the innovation and discussion of social enterprise business model among entrepreneurs, investors and other stakeholders. Second, the business model canvas of Osterwalder containing nine components is a good base for a business model platform with social enterprise.

2.2.1 Business Model Canvas

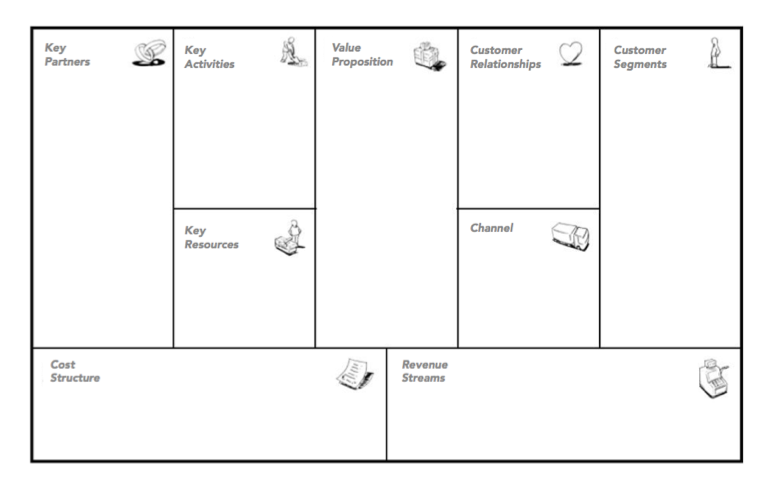

Osterwalder and Pigneur proposed a need for a shared language for entrepreneurs to discuss and describe their business models (Osterwalder, Pigneur, & Clark, 2010). In their book Business Model Generation, 470 practitioners from 45 countries together created the “Business Model Canvas” to facilitate much description and discussion on the topic. The Business Model Canvas has been applied and tested around the world and is already used by organizations such as IBM, Ericsson, Deloitte, the Public Works and Government Services of Canada, and many others. Osterwalder and Pigneur proposed that a business model could be best described through nine basic building blocks that show the logic of how a company intends to make money. The business model canvas and the definition of the nine building blocks are presented in figure 2 and table 4.

Osterwalder and Pigneur proposed a need for a shared language for entrepreneurs to discuss and describe their business models (Osterwalder, Pigneur, & Clark, 2010). In their book Business Model Generation, 470 practitioners from 45 countries together created the “Business Model Canvas” to facilitate much description and discussion on the topic. The Business Model Canvas has been applied and tested around the world and is already used by organizations such as IBM, Ericsson, Deloitte, the Public Works and Government Services of Canada, and many others. Osterwalder and Pigneur proposed that a business model could be best described through nine basic building blocks that show the logic of how a company intends to make money. The business model canvas and the definition of the nine building blocks are presented in figure 2 and table 4.

Figure 2. Business model canvas. Adapted from “Business model generation, ” by Osterwalder, Alexander, Pigneur, Yves, & Clark, Tim, 2010, Business model generation : a handbook for visionaries, game changers, and challengers, P44. Copyright © 2010 by Alexander Osterwalder.

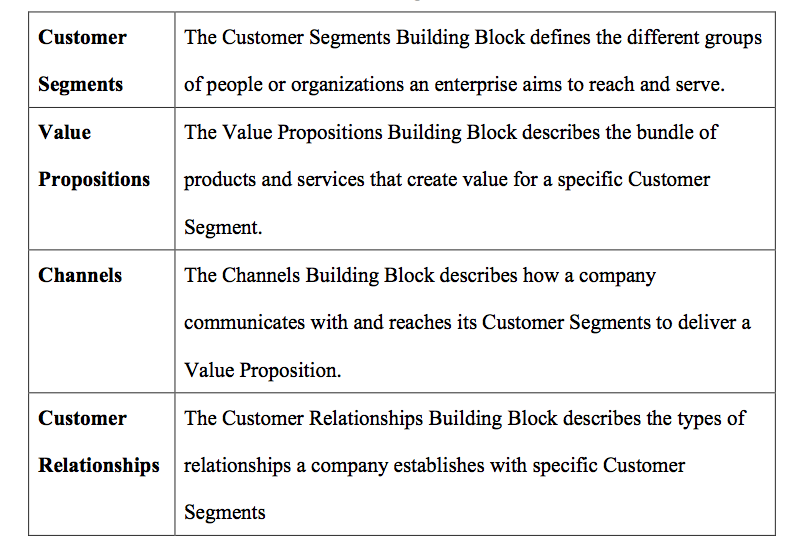

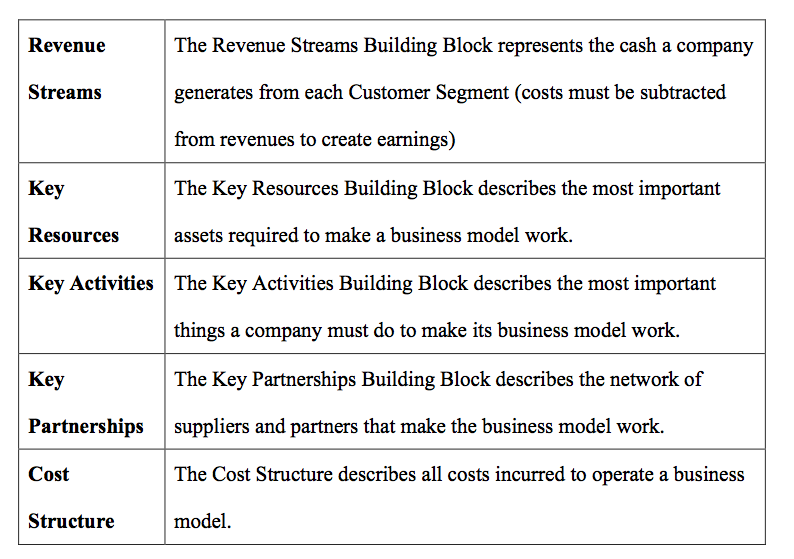

Table 4. Definitions of the nine building blocks in *business model canvas

Table 4. Definitions of the nine building blocks in *business model canvas

Note. *Business model canvas: a framework of business model consists of nine building blocks.

2.3 Designing Business Model for Social Enterprise

2.3.1 Non-for-profit Model

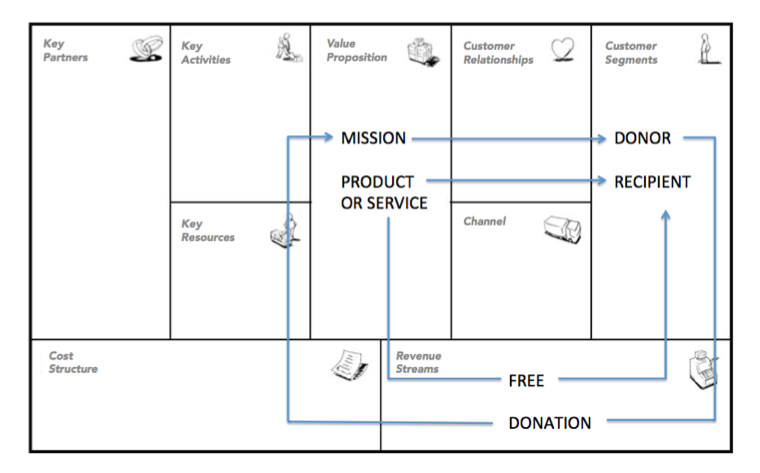

The “business model canvas” can also be applied to start-up businesses in addition to other for-profit corporations (Osterwalder et al., 2010). Although the word “business” may not be included in non-for-profit organization, the working bodies still bear and upkeep an impressive working business model. Every organization must generate enough revenue to cover its expenses in order to be sustainable. The major difference, however, is that these organizations have one more additional source of revenue. In third party founded NPOs, the sources of their revenue are from donations at individual, corporate, and government levels. Figure 3 shows the business model of third party founded NPOs.

2.3 Designing Business Model for Social Enterprise

2.3.1 Non-for-profit Model

The “business model canvas” can also be applied to start-up businesses in addition to other for-profit corporations (Osterwalder et al., 2010). Although the word “business” may not be included in non-for-profit organization, the working bodies still bear and upkeep an impressive working business model. Every organization must generate enough revenue to cover its expenses in order to be sustainable. The major difference, however, is that these organizations have one more additional source of revenue. In third party founded NPOs, the sources of their revenue are from donations at individual, corporate, and government levels. Figure 3 shows the business model of third party founded NPOs.

Figure 3. Non-for-profit Model. The recipients receive the product or service while the donors paid for the product or service. Adapted from “Business model generation, ” by Osterwalder, Alexander, Pigneur, Yves, & Clark, Tim, 2010, Business model generation : a handbook for visionaries, game changers, and challengers, P264. Copyright © 2010 by Alexander Osterwalder.

Since the 2009 financial crisis, however, individual and corporate donations have been decreasing dramatically and freezing much over time. Ever since the beginning of the European debt crisis, the governments of many countries across the world have begun various austerity measures, slashing government spending on many social programs. Some NPOs traditionaly founded by third party sponsors changes their revenue collecting policies, changing with the times. Understanding that government subsidies may no longer be necessarily guaranteed, they began to rely solely on third party founding. However, during the recent financial crisis, these NPOs have shown to be financially unstable and unsustainable.

Born out of this new financial era, a new business model is immerging, that is, they are following the triple-bottom-line business model. The triple bottom-line business model pursues its social and environmental goals simultaneously to generating revenues without any outside sponsors or donorships (Elkington, 1998). This shows in many ways that organizations with social or environmental goals no longer have to worry about the changing tide of its donations and subsidies dollars.

2.3.2 Triple bottom-line business model

In 1997, British scholar John Elkington developed the concept of the triple bottom line, which has since then revolutionized businesses, nonprofits and governments measure sustainability and the performance of projects or policies (Slaper & Hall, 2011). The TBL is an accounting framework that incorporates three dimensions of performance: social, environmental, and financial performance. This framework differs from traditional reporting frameworks as it includes environmental and social measures that are more than often difficult to be assigned appropriate means of measurement (Elkington, 1998)

The most significant difference between a for-profit corporation and an organization run by the triple bottom-line business model is that the central goal of the enterprise has changed. The goal of traditional for-profit corporation is maximizing the shareholder’s interest. Conversely, the working goal of triple bottom-line organization is to expand one’s range not only to account for a continued and sustainable financial base but also for continued collaboration towards solving social woes and environmental concerns.

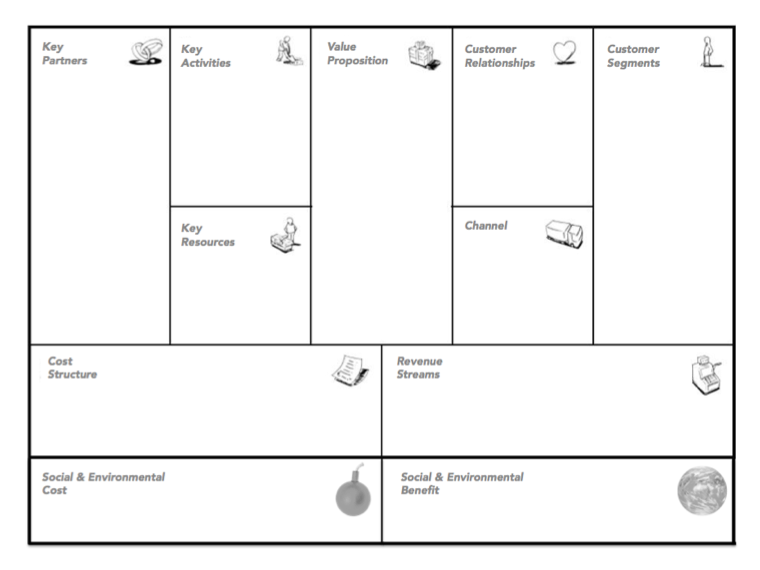

To design a business model that well corresponds with the goal of a triple bottom-line, the business model canvas must be expanded with two additional building blocks, namely, “Social and Environmental Revenue” and “Social and Environmental Costs” (Osterwalder et al., 2010). Figure 4 demonstrates the expanded business model canvas of Triple bottom line business model.

Since the 2009 financial crisis, however, individual and corporate donations have been decreasing dramatically and freezing much over time. Ever since the beginning of the European debt crisis, the governments of many countries across the world have begun various austerity measures, slashing government spending on many social programs. Some NPOs traditionaly founded by third party sponsors changes their revenue collecting policies, changing with the times. Understanding that government subsidies may no longer be necessarily guaranteed, they began to rely solely on third party founding. However, during the recent financial crisis, these NPOs have shown to be financially unstable and unsustainable.

Born out of this new financial era, a new business model is immerging, that is, they are following the triple-bottom-line business model. The triple bottom-line business model pursues its social and environmental goals simultaneously to generating revenues without any outside sponsors or donorships (Elkington, 1998). This shows in many ways that organizations with social or environmental goals no longer have to worry about the changing tide of its donations and subsidies dollars.

2.3.2 Triple bottom-line business model

In 1997, British scholar John Elkington developed the concept of the triple bottom line, which has since then revolutionized businesses, nonprofits and governments measure sustainability and the performance of projects or policies (Slaper & Hall, 2011). The TBL is an accounting framework that incorporates three dimensions of performance: social, environmental, and financial performance. This framework differs from traditional reporting frameworks as it includes environmental and social measures that are more than often difficult to be assigned appropriate means of measurement (Elkington, 1998)

The most significant difference between a for-profit corporation and an organization run by the triple bottom-line business model is that the central goal of the enterprise has changed. The goal of traditional for-profit corporation is maximizing the shareholder’s interest. Conversely, the working goal of triple bottom-line organization is to expand one’s range not only to account for a continued and sustainable financial base but also for continued collaboration towards solving social woes and environmental concerns.

To design a business model that well corresponds with the goal of a triple bottom-line, the business model canvas must be expanded with two additional building blocks, namely, “Social and Environmental Revenue” and “Social and Environmental Costs” (Osterwalder et al., 2010). Figure 4 demonstrates the expanded business model canvas of Triple bottom line business model.

Figure 4. Triple bottom-line business model. Beside the original nine building blocks, two new building blocks: “Social and Environmental Revenue” and “Social and Environmental Costs” are incorporated in the triple bottom-line business model.

In the business model framework developed in my thesis, “Social and Environmental Revenue” and “Social and Environmental Costs” are defined and assessed by social impact assessment (SIA) and environmental impact assessment (EIA). "Social impact assessment includes the processes of analyzing, monitoring and managing the intended and unintended social consequences, both positive and negative, of planned interventions (policies, programs, plans, projects) and any social change processes invoked by those interventions. Its primary purpose is to “bring about a more sustainable and equitable biophysical and human environment” (Vanclay, 2003). On the other hand, environmental impact assessment is defined as “the process of identifying, predicting, evaluating and mitigating the biophysical, social, and other relevant effects of development proposals prior to major decisions being taken and commitments made” (Glasson, Therivel, & Chadwick, 1999). A business model may have possible positive or negative impacts on the environment, consisting of the environmental, social and economic aspects.

2.3.3 Social enterprise business model

In designing a triple bottom-line business model, one cannot neglect to describe the most important asset of a social enterprise—people. All other factors such as channel and value proposition are key partners are important, but none can make an organization more successful that the cooperation and collaboration that people provide.

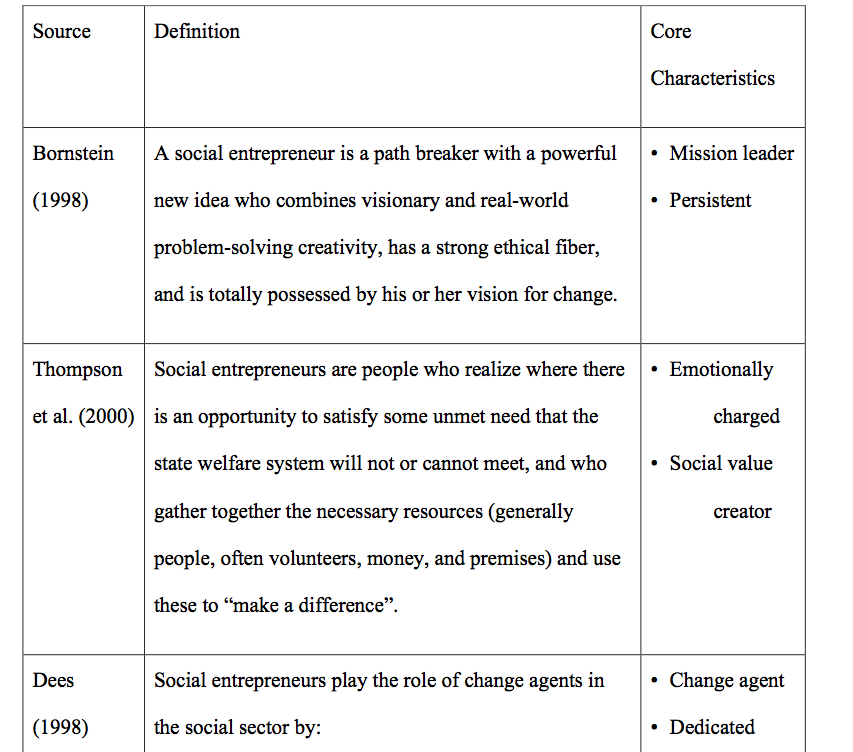

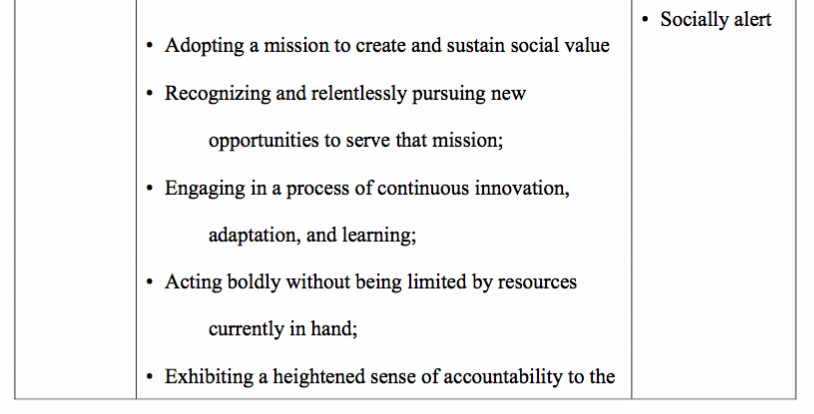

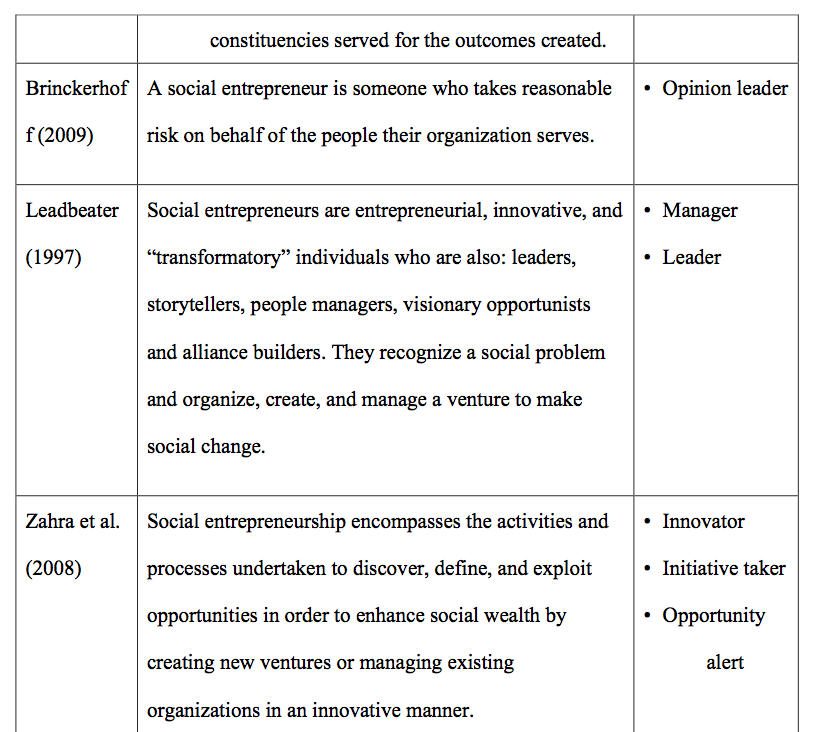

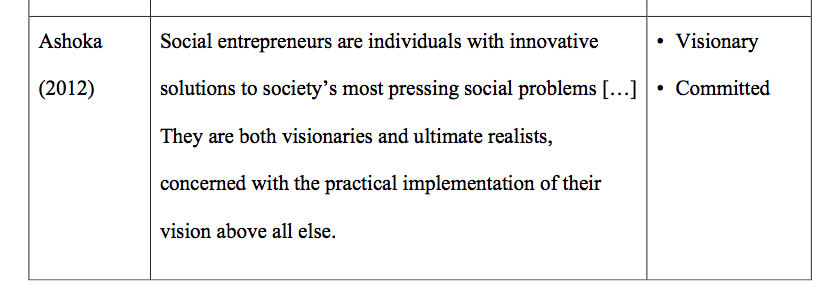

The social entrepreneur is a mission-driven individual who uses a set of entrepreneurial faculties to deliver a social value to the less privileged or those in concerned situations, all through an entrepreneurially oriented entity that is financially independent, self-sufficient, or sustainable, or all of more than one of the above (Abu-Saifan, 2012). The Contrasting definitions and core characteristics of the terms “social entrepreneur” are sorted in table 5.

Table 5. Contrasting definitions and core characteristics of the terms “social entrepreneur”.

In the business model framework developed in my thesis, “Social and Environmental Revenue” and “Social and Environmental Costs” are defined and assessed by social impact assessment (SIA) and environmental impact assessment (EIA). "Social impact assessment includes the processes of analyzing, monitoring and managing the intended and unintended social consequences, both positive and negative, of planned interventions (policies, programs, plans, projects) and any social change processes invoked by those interventions. Its primary purpose is to “bring about a more sustainable and equitable biophysical and human environment” (Vanclay, 2003). On the other hand, environmental impact assessment is defined as “the process of identifying, predicting, evaluating and mitigating the biophysical, social, and other relevant effects of development proposals prior to major decisions being taken and commitments made” (Glasson, Therivel, & Chadwick, 1999). A business model may have possible positive or negative impacts on the environment, consisting of the environmental, social and economic aspects.

2.3.3 Social enterprise business model

In designing a triple bottom-line business model, one cannot neglect to describe the most important asset of a social enterprise—people. All other factors such as channel and value proposition are key partners are important, but none can make an organization more successful that the cooperation and collaboration that people provide.

The social entrepreneur is a mission-driven individual who uses a set of entrepreneurial faculties to deliver a social value to the less privileged or those in concerned situations, all through an entrepreneurially oriented entity that is financially independent, self-sufficient, or sustainable, or all of more than one of the above (Abu-Saifan, 2012). The Contrasting definitions and core characteristics of the terms “social entrepreneur” are sorted in table 5.

Table 5. Contrasting definitions and core characteristics of the terms “social entrepreneur”.

Note. From “Social Entrepreneurship: Definition and Boundaries,” by Abu-Saifan, Samer, 2012, Technology Innovation Management Review (February 2012: Technology Entrepreneurship) p.24

The interest of social entrepreneurs have to engage in their field of work stems from their role in addressing critical social problems and their dedication in improving the well being of society (Zahra, Rawhouser, Bhawe, Neubaum, & Hayton, 2008). When comparing the characteristics of other entrepreneurs with social entrepreneurs, one might notice that the ultimate goal of an entrepreneur is to create economic wealth, whereas the ultimate priority is to satisfy their social mission. Social entrepreneurs design their revenue-generating strategies to serve their mission directly and to deliver social value to those deserving (Abu-Saifan, 2012).

To assist the social venture capitalist even better, evaluate social enterprise, and help social entrepreneurs better present themselves, representing the “social entrepreneur” through a business model canvas uniquely designed for them is indispensible and invaluable.

The interest of social entrepreneurs have to engage in their field of work stems from their role in addressing critical social problems and their dedication in improving the well being of society (Zahra, Rawhouser, Bhawe, Neubaum, & Hayton, 2008). When comparing the characteristics of other entrepreneurs with social entrepreneurs, one might notice that the ultimate goal of an entrepreneur is to create economic wealth, whereas the ultimate priority is to satisfy their social mission. Social entrepreneurs design their revenue-generating strategies to serve their mission directly and to deliver social value to those deserving (Abu-Saifan, 2012).

To assist the social venture capitalist even better, evaluate social enterprise, and help social entrepreneurs better present themselves, representing the “social entrepreneur” through a business model canvas uniquely designed for them is indispensible and invaluable.